Alternative Data • June 2019

Blog Post

A few days after I registered listening247 on alternativedata.org (a spur of the moment kind of thing), companies I had never even heard of before started reaching out to explore cooperation. One of them was Bloomberg. Obviously they were an exception - I did happen to know them.

The unknown (to me) companies were mainly conference organisers fishing for alternative data providers, to bring them together with investment funds... So we bit.

Our first question as you may imagine, was: what is alternative data? They said that there are many categories such as sentiment from social and news, app usage, surveys, satellite imagery, geo-location etc. and their main use is to give investors an edge in predicting stock prices.

Funnily enough, they all used the same example to bring their point home: satellite images of retailer parking lots, that depending on how full they are, can predict the retailer’s sales and share against competitors. I have to admit, even though it’s a bit out there it does make sense.

Traditionally investment funds and other traders use fundamentals to make their investment decisions. Even though alternative data and the ability to analyse it (using machine learning) have been around for over a decade, in the last 12 months - i have the impression - chatter about it is going through the roof.

I am thinking: “looks like we caught this wave quite early”.

One of my favourite business success analogies is 'the surfer'; for the act of surfing, 3 things are required: a surfer, a surfboard and a wave. The surfer is the CEO of a company, the surfboard the company itself, and both are waiting for the mother of all waves to lift and accelerate them. Without the wave, even the best CEO with the best functioning company will not make it far.

Needless to say, we jumped in with both feet.

Next order of business was to figure out for ourselves to what extent our “alternative data” correlates with stock prices. It so happened that when all this interest became apparent we were considering to focus on social intelligence for the banking sector; so when a well known business school asked us if we wanted to investigate the correlation of Bank Governance stories in online news and social media to their business performance we knew exactly what needed to be done.

If you are a regular reader of our articles you will already know the scope of the social intelligence project we carried out:

- Keywords for harvesting: 11 major brands including HSBC, Barclays, RBS, Deutsche Bank etc.

- Language: English

- Geography: Global

- Time Period: 1st May 2018 - 30th April 2019

- Data sources: Twitter, blogs, boards / forums, news, reviews, videos

- Machine learning annotations: sentiment, topics, brands, and "noise" (irrelevant posts picked up due to homonyms)

The data scientists and researchers of listening247, after having cleaned the data from “noise”, annotated each post with topics and sentiment using custom machine learning models. The sentiment, semantic and brand accuracy were all above 80%.

They then regressed the daily stock price of the banks against various time series derived from the annotated posts that were harvested.

The results were astounding!

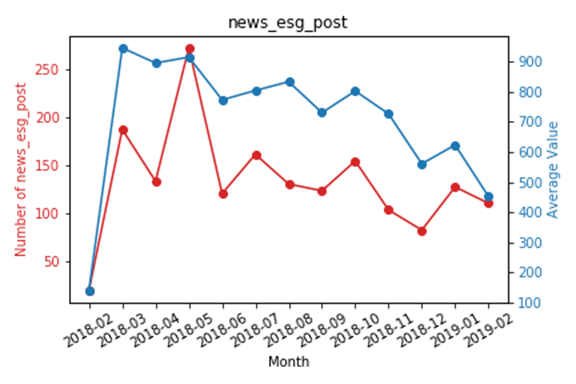

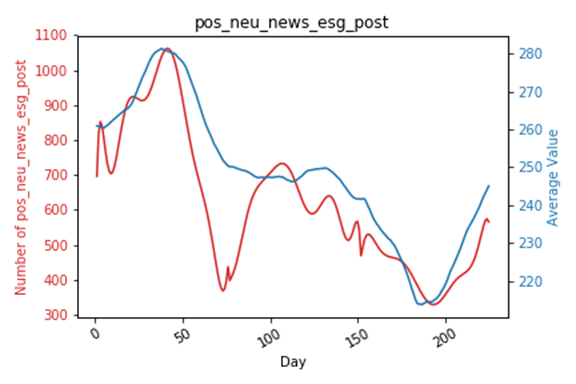

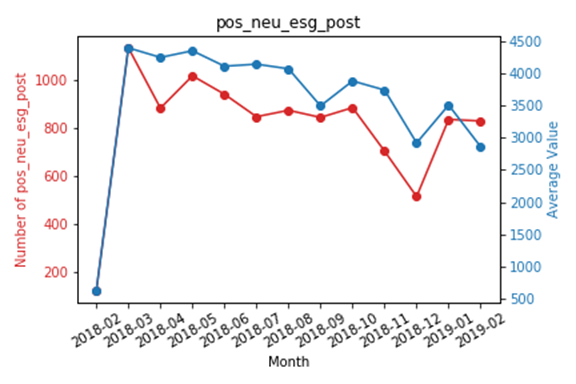

For each of the 4 examples below I will describe the social intelligence metrics that were correlated with daily bank valuation. As with all R&D projects there was a lot of trial and error going on. What was impressive…….hmmm, I will not give this away yet.

Fig 1.

Fig 2.

Fig 3.

Fig 4.

Amazing! Our alternative data turns out to be quite useful primarily to discretionary, and private equity and with a few adjustments to quantitative funds. It feels like the sky is the limit. We probably need to create a new business unit to deal exclusively with the 15 social intelligence metrics that we discovered to date.

Please do reach out and share your views or questions @listening247, mmichael@listening247.com if you find this interesting.

Our contact details

Name: DigitalMR Ltd ( dba. DMR)

Address: Liberty House, 222 Regent Street, W1B 5TR, London, United Kingdom

Phone Number: 0044 203 795 4715

E-mail: info@digital-mr.com

This privacy policy was completed on 20th October 2023.

The type of personal information we collect:

We currently collect and process the following information:

Personal identifiers, contacts and characteristics (for example, name and contact details)

How we get the personal information and why we have it

Most of the personal information we process is provided to us directly by you for one of the following reasons:

We also receive personal information indirectly, from the following sources in the following scenarios:

We use the information that you have given us for:

We may share this information:

The provisions below set out the main circumstances in which DMR may disclose personal information to third parties.

DMR also disclose individually identified information to a third party in the following instances:

In addition, DMR reserves the right to allow access to DMR's systems to third parties providing technical services to DMR when such access is required to provide those services and to provide individually identifiable information to third parties who provide services on DMR's behalf. DMR require such third parties to maintain the security of personally identifiable information and use it only on DMR's behalf in connection with the provision of such services.

DMR may share the collected data along with any other relevant information which is available to the public with clients anonymously.

DMR may also disclose personally identifiable information as required by law or a competent regulatory authority.

If a government authority asks us to share information:

DMR may provide anonymous information and aggregated data about the usage of DMR's services to third parties for such purposes as DMR deems, in DMR's sole discretion, to be appropriate, but this will not include information that can be used to identify the individual.

No individual may disclose personally identifiable information to any third party unless it is with DMR's and any other relevant party's consent.

DMR never sells or shares personally identifiable information with third parties for their marketing purposes.

Third Party Processors

Our carefully selected partners and service providers may process personal information about you on our behalf as described below:

Under the UK General Data Protection Regulation (UK GDPR), the lawful bases we rely on for processing this information are:

Address: Liberty House, 222 Regent Street, W1B 5TR, London, United Kingdom

Phone Number: 0044 203 795 4715

E-mail: info@digital-mr.com

How we store your personal information

Your information is securely stored.

The security of personally identifiable information is a priority for DMR. DMR employs security measures to protect such information both online and offline from access by unauthorised persons and against unlawful processing, accidental loss, destruction and damage.

In particular, note that DMR may require (or be required) to retain certain data if it may be necessary to prevent fraud or future abuse, or for legitimate business purposes, such as analysis of aggregated, non-personally identifiable data if required for regulatory compliance purposes, or if otherwise required by law. All retained data will continue to be subject to the terms of this privacy.

We keep personal information for as long as a project is live and after that for at least 5 years. We will then dispose of your information by deleting the electronic files that contain it. Archived backups might be stored for another 5 years.

DMR will retain the information as long as the law requires. We will then dispose of personal information by deleting the data from our servers.

Your data protection rights

Under data protection law, you have rights including:

Your right of access - You have the right to ask us for copies of your personal information.

Your right to rectification - You have the right to ask us to rectify personal information you think is inaccurate. You also have the right to ask us to complete information you think is incomplete.

Your right to erasure - You have the right to ask us to erase your personal information in certain circumstances.

Your right to restriction of processing - You have the right to ask us to restrict the processing of your personal information in certain circumstances.

Your right to object to processing - You have the right to object to the processing of your personal information in certain circumstances.

Your right to data portability - You have the right to ask that we transfer the personal information you gave us to another organisation, or to you, in certain circumstances.

You are not required to pay any charge for exercising your rights. If you make a request, we have one month to respond to you.

Please contact us using the information below if you wish to make a request.

Address: Liberty House, 222 Regent Street, W1B 5TR, London, United Kingdom

Phone Number: 0044 203 795 4715

E-mail: info@digital-mr.com

How to complain

If you have any concerns about our use of your personal information, you can make a complaint to us at:

Address: Liberty House, 222 Regent Street, W1B 5TR, London, United Kingdom

Phone Number: 0044 203 795 4715

E-mail: info@digital-mr.com

You can also complain to the ICO if you are unhappy with how we have used your data.

The ICO’s address:

Information Commissioner’s Office

Wycliffe House

Water Lane

Wilmslow

Cheshire

SK9 5AF

Helpline number: 0303 123 1113

ICO website: https://www.ico.org.uk